IntelliPaper

Abstract

Federated data governance enables banking institutions to leverage collaborative capabilities, effectively combating money laundering activities while upholding compliance requirements and safeguarding information autonomy. The structural design merges secure information warehousing with cognitive systems, creating identification frameworks that maintain confidentiality across institutional boundaries. Utilizing federated learning principles, institutions uncover intricate laundering schemes typically concealed within segregated systems. The governance structure employs cryptographic safeguards, detailed permission hierarchies, and permanent verification records to protect information throughout collaborative engagements. Successful deployment addresses system interoperability, allocates processing capacity, and harmonizes data structures among participating organizations. Regulatory aspects include navigating jurisdictional requirements, transnational information exchange protocols, and coherence with global financial security standards. The article yields improvements in identification precision, surveillance capabilities, and notification accuracy when compared with conventional isolated approaches. Financial organizations implementing federated governance enhance compliance positions while sustaining operational autonomy. Through a balance between security imperatives and functional requirements, this architecture provides a comprehensive solution to coordinated anti-money laundering challenges within interconnected financial markets, laying the groundwork for productive collaboration against increasingly sophisticated financial offenses.

Explore Digital Article Text

I. INTRODUCTION

Financial organizations face increasingly intricate money laundering techniques, necessitating joint detection strategies spanning institutional boundaries. The supervisory environment governing financial crime prevention has transformed considerably, creating expanded responsibilities for client verification, transaction surveillance, and suspicious behavior documentation. Contemporary regulatory structures prioritize measurable results over procedural adherence, redirecting organizational attention toward quantifiable achievements in illicit finance prevention [1]. This shifting emphasis presents considerable difficulties for organizations operating with conventional isolated monitoring systems confined by corporate limitations. Oversight requirements throughout major financial regions simultaneously promote intelligence sharing while mandating rigorous privacy safeguards, resulting in apparent inconsistencies for compliance professionals managing these conflicting directives. Information exchange restrictions constitute formidable obstacles to productive cross-institutional money laundering identification capabilities. Financial institutions uphold extensive confidentiality duties concerning customer data, restricting allowable disclosure circumstances without clear authorization or particular regulatory allowances.

These constraints derive from multiple sources, including data protection legislation, financial privacy regulations, contractual obligations, and jurisdictional variations in information sharing permissions . The resulting fragmentation creates substantial advantages for sophisticated money laundering operations that deliberately structure activities across multiple institutions to avoid detection thresholds. Traditional approaches to addressing these constraints through centralized information repositories introduce significant vulnerabilities regarding unauthorized access, create single points of failure, and frequently encounter jurisdictional limitations preventing comprehensive implementation. Federated approaches to anti-money laundering detection offer promising resolution pathways addressing both collaboration necessities and privacy protection requirements.

These methodologies establish frameworks enabling collective intelligence development without requiring underlying data consolidation, fundamentally transforming cross-institutional cooperation possibilities. Implementation architectures typically establish distributed processing capabilities, maintaining institutional data sovereignty while enabling collaborative analytical functions through careful orchestration of protected information exchanges . Advanced implementations incorporate cryptographic protections, ensuring information security throughout collaborative processes while maintaining comprehensive audit capabilities, addressing regulatory verification requirements.

These approaches demonstrate particular effectiveness in addressing complex laundering methodologies deliberately fragmented across multiple institutions, detecting patterns invisible within isolated monitoring systems. Financial institutions implementing federated detection frameworks report substantial improvements in suspicious activity identification while simultaneously strengthening privacy protection capabilities and regulatory compliance positions.

Table 1: Industry Applications of Federated Data Governance [2,8]

| Industry | Implementation Benefits | Strategic Outcomes |

| Healthcare | Clinic-specific data control while maintaining HIPAA compliance | Enhanced patient privacy with streamlined information access |

| Hospitality | Property-level management within corporate standards | Consistent brand experience with location-specific customization |

| Finance | Department-specific security protocols with controlled sharing | Improved customer service while maintaining compliance |

| Agriculture | Farm-specific data sovereignty with industry benchmarking | Optimized local operations with collaborative insights sharing |

Today's banking system struggles against increasingly clever money laundering schemes that deliberately span multiple institutions. Criminal networks split their financial maneuvers across different banks, ensuring each piece looks innocent when viewed alone. By carefully keeping transactions under warning thresholds at individual institutions, these operations create patterns visible only when examining data across organizational boundaries. This fragmentation creates fundamental limitations for traditional monitoring approaches confined within individual institutional perimeters. Banking organizations consequently struggle to fulfill expanding regulatory mandates while operating with inherently incomplete information visibility [1].

The regulatory landscape governing financial crime prevention has shifted substantially, emphasizing outcomes rather than procedural compliance. This reorientation creates significant implementation hurdles for institutions operating with conventional, siloed detection systems. Oversight frameworks across major jurisdictions simultaneously encourage intelligence sharing while imposing stringent privacy requirements, creating apparent contradictions for compliance teams navigating these competing directives .

1.1 Background and Financial Industry Challenges

Banks face stringent privacy duties that sharply curtail when and how they may share client data with outside parties. Without clear customer consent or narrowly defined regulatory allowances, such exchanges remain largely prohibited. This restrictive environment springs from overlapping legal frameworks – privacy laws, banking secrecy provisions, client agreements, and widely varying rules across different countries all combine to create formidable barriers around customer information . The resulting constraints provide substantial advantages to sophisticated laundering operations that deliberately structure activities across multiple financial organizations.

Traditional resolution approaches through centralized information repositories introduce significant vulnerabilities regarding unauthorized access, create single points of failure, and frequently encounter jurisdictional boundaries that prevent comprehensive implementation. Banking organizations consequently implement conservative interpretation frameworks regarding information sharing permissions, prioritizing privacy compliance over potential detection effectiveness improvements .

These cautious orientations create substantial advantages for money laundering networks that deliberately structure operations across institutional boundaries. Pattern recognition capabilities remain fundamentally constrained by incomplete visibility, preventing effective identification of deliberately fragmented activities remaining below individual monitoring thresholds. Specialized detection algorithms demonstrate limited effectiveness without comprehensive contextual information spanning organizational boundaries [2].

The financial industry consequently faces a structural dilemma: improving detection capabilities requires enhanced information sharing, yet sharing itself introduces substantial privacy and security risks that banking organizations cannot accept. This central tension drives exploration of alternative approaches, enabling collaborative intelligence development without requiring underlying data consolidation.

1.2 Hypothesis and Collaborative Solution Framework

The governing hypothesis behind federated governance approaches proposes that financial institutions can dramatically improve money laundering detection effectiveness through collaborative model development without exposing sensitive customer data. This hypothesis suggests that distributed learning frameworks enable pattern recognition across institutional boundaries while maintaining strict data locality, fundamentally transforming cross-organizational cooperation possibilities [1]. The solution framework addresses this hypothesis through specialized architectures establishing distributed processing capabilities while preserving institutional data sovereignty. These frameworks typically implement cryptographic protection mechanisms, ensuring information security throughout collaborative processes while maintaining comprehensive audit capabilities addressing regulatory verification requirements [2].

Core architectural principles include data minimization, purpose limitation, and provable security guarantees that collectively transform previously impossible collaboration scenarios into practical implementation possibilities. The resulting frameworks demonstrate particular effectiveness in addressing complex laundering methodologies deliberately fragmented across multiple institutions, detecting patterns invisible within isolated monitoring systems .

Financial organizations implementing these approaches report substantial improvements in suspicious activity identification while simultaneously strengthening privacy protection capabilities and regulatory compliance positions. The distributed intelligence development methodology preserves essential institutional autonomy while enabling unprecedented cooperation against increasingly sophisticated financial crime networks . This architectural approach fundamentally transforms cross-institutional cooperation possibilities by eliminating traditional barriers regarding sensitive information sharing. Through careful orchestration of protected information exchanges and distributed learning methodologies, banking organizations establish collective detection capabilities without compromising essential confidentiality obligations.

II. CURRENT CHALLENGES IN CROSS-INSTITUTIONAL AML SYSTEMS

Financial institutions confront substantial data privacy constraints when developing cross-institutional anti-money laundering capabilities. Regulatory frameworks establish comprehensive requirements regarding customer information protection, creating significant compliance challenges for collaborative detection initiatives. These requirements typically prohibit sharing personally identifiable information without explicit authorization exemptions, limiting potential cooperation scenarios [3]. Jurisdictional variations further complicate implementation efforts, with multinational institutions navigating inconsistent regulatory requirements regarding permissible information exchanges. Recent legislative developments, including enhanced data protection frameworks, introduce additional complexity through expanded individual rights regarding information processing limitations. Financial institutions consequently implement conservative interpretation approaches regarding information sharing permissions, prioritizing privacy compliance over potential detection effectiveness improvements. This cautious orientation creates substantial advantages for money laundering operations deliberately structured to exploit visibility limitations between institutions. Technical barriers to secure information sharing compound regulatory challenges, further restricting cross-institutional detection capabilities. Legacy infrastructure deployed within many financial institutions lacks interoperability capabilities necessary for seamless information exchange, requiring substantial modification for meaningful collaboration [4].

Security concerns regarding data transmission vulnerabilities, unauthorized access risks, and potential breach implications create additional implementation obstacles. Architectural inconsistencies between institutional systems introduce compatibility challenges regarding data formats, semantic interpretations, and processing methodologies. Implementation costs represent significant considerations, particularly for smaller institutions with limited technology investment capabilities. These technical limitations frequently result in manual information exchange processes lacking scalability for comprehensive transaction monitoring applications. Without systematic addressing of these foundational technical barriers, regulatory permissions alone prove insufficient for effective cross-institutional detection implementations.

Isolated detection systems demonstrate fundamental limitations regarding sophisticated laundering methodologies spanning multiple financial institutions.

Pattern recognition capabilities remain constrained by incomplete visibility, preventing effective identification of deliberately fragmented activities designed to remain below individual institutional monitoring thresholds [3]. False positive rates within isolated systems remain substantially elevated due to contextual information limitations, creating significant resource allocation inefficiencies within compliance operations. Typology detection capabilities demonstrate particular weaknesses regarding coordinated laundering operations utilizing multiple organizational relationships to obscure ultimate beneficial ownership structures. These limitations create substantial vulnerabilities within the financial system despite significant institutional investments in compliance operations and monitoring technologies [4]. These surveillance deficiencies allow complex illicit networks to maintain activities despite strengthened oversight mandates and organizational detection investments. Resolving such inherent constraints demands a comprehensive reimagining of conventional financial crime prevention structures, developing systems facilitating productive institutional cooperation while preserving essential confidentiality safeguards and regulatory adherence.

Banks increasingly find themselves caught between contradictory demands from oversight bodies. On one hand, regulators insist on catching more laundered money moving through the financial system; on the other, they strictly enforce customer confidentiality rules. This squeeze places compliance officers in a nearly impossible position – expected to spot criminal patterns while barred from sharing the very information needed to recognize them. Traditional approaches to anti-money laundering monitoring suffer from inherent limitations when addressing sophisticated criminal operations deliberately spanning multiple financial institutions. Detection systems confined within organizational boundaries cannot identify patterns specifically designed to exploit these structural blind spots [3].

Regulatory frameworks create additional complexity through inconsistent information-sharing provisions across jurisdictions. European institutions operate under GDPR constraints that differ substantially from Asia-Pacific regional requirements, which themselves vary from North American frameworks. These divergent regulations force multinational financial institutions to implement patchwork solutions with varying capabilities across geographic operations. Even within shared regulatory zones, interpretation differences between institutions create additional barriers to meaningful collaboration [4].

2.1 Critical Obstacles in AML Implementation

Even where regulatory permission exists, banks face stubborn technical hurdles impeding collaboration. Core banking platforms purchased and customized over many years speak different digital languages, organize information using conflicting classification systems, and exchange data through mismatched connection methods. Financial institutions operate complex technology ecosystems comprising hundreds of applications accumulated through decades of organizational evolution and acquisition activity. These fragmented environments create substantial integration challenges when attempting to establish cross-institutional communication channels .

Security considerations compound these difficulties, with institutions justifiably concerned about unauthorized access risks during information exchange processes. Banking security teams operate under worst-case scenario planning regarding data exposure, recognizing that financial data represents particularly attractive targets for malicious actors. Without robust protection mechanisms demonstrating mathematical guarantees around information security, risk management frameworks typically reject information sharing proposals regardless of potential detection benefits .

Beyond technical limitations, significant operational obstacles emerge from differing institutional approaches to transaction monitoring. Divergent risk appetites, business models, and customer bases create natural variations in how banks categorize and investigate unusual activities. These differences manifest in inconsistent typology definitions, alert thresholds, and investigation protocols. Such variations create substantial challenges when attempting to establish common frameworks supporting cross-institutional pattern recognition [3].

Resource asymmetry between financial institutions further complicates collaborative efforts. Major global banks maintain sophisticated compliance operations with substantial technology investments, while smaller regional institutions operate with limited dedicated resources. These capability differences create practical implementation challenges regarding computational burden distribution, technical expertise requirements, and participation costs that frequently derail well-intentioned collaboration initiatives [4].

Table 2: Federated vs. Centralized Data Systems [1,7]

| Aspect | Federated Data Systems | Centralized Data Systems |

| Ownership | Domain-specific teams control within enterprise standards | A single authority governs all data assets |

| Decision-Making | Distributed with local optimization capabilities | Consolidated with standardized implementation |

| Complexity | Higher initial coordination, simpler ongoing maintenance | Lower initial deployment, higher long-term management |

| Scalability | Modular expansion accommodating organizational growth | Requires restructuring during significant changes |

| Flexibility | Responsive to domain-specific requirements | Consistent practices with limited customization |

| Organizational Fit | Optimal for decentralized operations with diverse needs | Suited for hierarchical structures with uniform processes |

2.2 Financial Impact of Fragmented AML Approaches

The financial consequences of continuing with isolated monitoring approaches extend far beyond compliance costs. Banking institutions collectively spend billions annually on transaction surveillance systems, investigation teams, and regulatory reporting mechanisms – yet criminal networks continue exploiting visibility gaps to move illicit funds through the global financial system. This persistent vulnerability creates substantial direct costs through regulatory penalties imposed on institutions deemed to have inadequate detection capabilities .

Beyond explicit fines, banking organizations face significant indirect financial impacts through increased capital requirements imposed on institutions with identified compliance deficiencies. These additional capital allocations represent substantial opportunity costs, preventing deployment of those resources toward productive lending activities, generating direct revenue. Regulatory enforcement actions frequently include business restrictions limiting growth opportunities until remediation activities reach satisfactory completion .

Reputation damage presents another significant financial risk, with public disclosure of compliance failures creating lasting market perception challenges. Institutions identified with major money laundering incidents experience measurable impacts across multiple financial dimensions – customer acquisition costs increase, funding expenses rise through higher risk premiums, and market valuation multiples contract relative to peers without similar incidents [3].

From an efficiency perspective, isolated approaches create substantial wasteful duplication across the financial ecosystem. Each institution independently maintains detection systems, investigation teams, and compliance specialists – creating economy-wide inefficiency through redundant capabilities addressing identical typologies. These duplicated expenses ultimately reflect in higher costs passed on to customers through fee structures and lending rates while delivering suboptimal detection effectiveness .

The indirect societal costs of inadequate money laundering detection extend beyond institutional impacts to facilitate criminal enterprises ranging from narcotics trafficking to human smuggling, creating profound damages that financial institutions have an ethical responsibility to help prevent. As regulatory expectations continue escalating, banking organizations face growing urgency to develop more effective approaches balancing information utility with appropriate privacy protections .

III. FEDERATED DATA GOVERNANCE FRAMEWORK DESIGN

Developing robust federated data governance frameworks for laundering prevention demands thorough structural blueprints addressing system compatibility, protection mechanisms, and regulatory adherence specifications. Metadata harmonization constitutes an essential building block facilitating significant information transfer between organizations while preserving contextual integrity. These standardization efforts typically encompass transaction categorization taxonomies, entity identification protocols, and risk classification frameworks aligned with international standards . Financial institutions participating in federated governance structures implement translation layers mapping proprietary data structures to agreed exchange formats, preserving internal system integrity while enabling cross-institutional analysis. Standardized attribute definitions establish contextual meaning consistency, preventing misinterpretation during collaborative analytical processes. Exchange protocols incorporate cryptographic verification mechanisms, ensuring data integrity throughout transmission processes while maintaining complete audit trails for regulatory verification purposes.

Virtualized data warehouse architectures provide technological foundations supporting federated governance implementation without requiring physical data consolidation. These architectures establish secure query interfaces enabling analytical processes across distributed repositories while maintaining institutional data sovereignty. Advanced implementations incorporate distributed ledger technologies, creating immutable access records while facilitating multi-party authorization workflows . The virtualization layer typically integrates with existing institutional data infrastructure through secure API frameworks, minimizing implementation complexity while preserving investments in established systems.

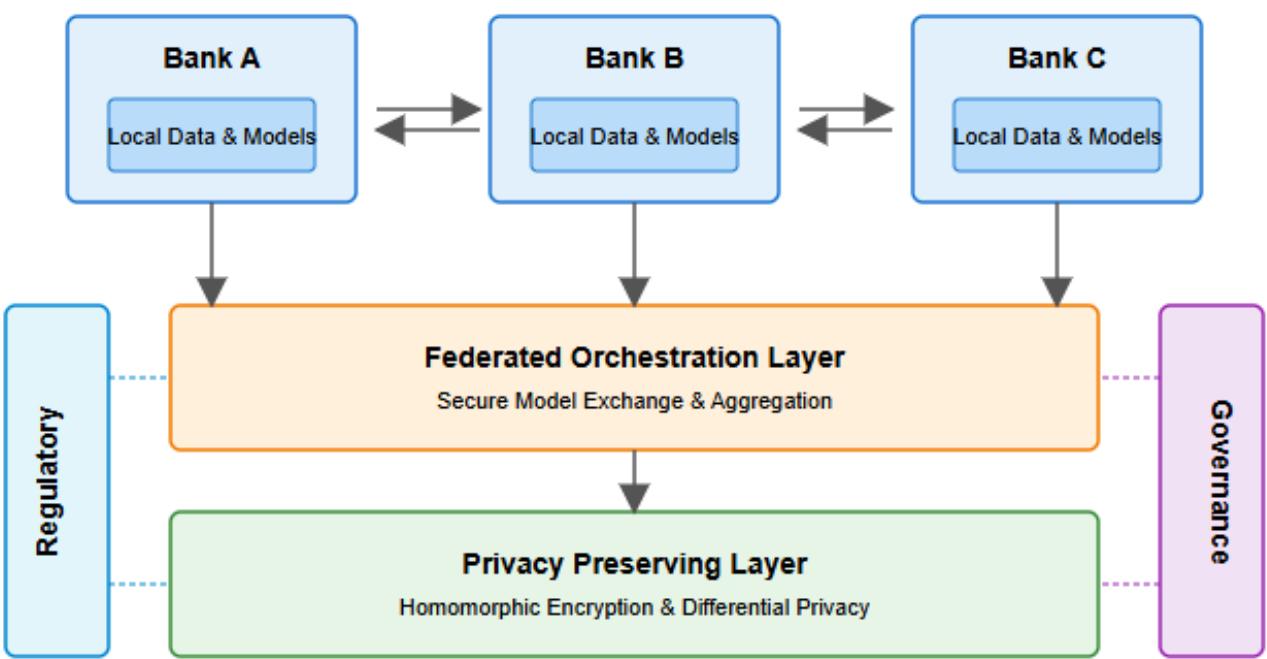

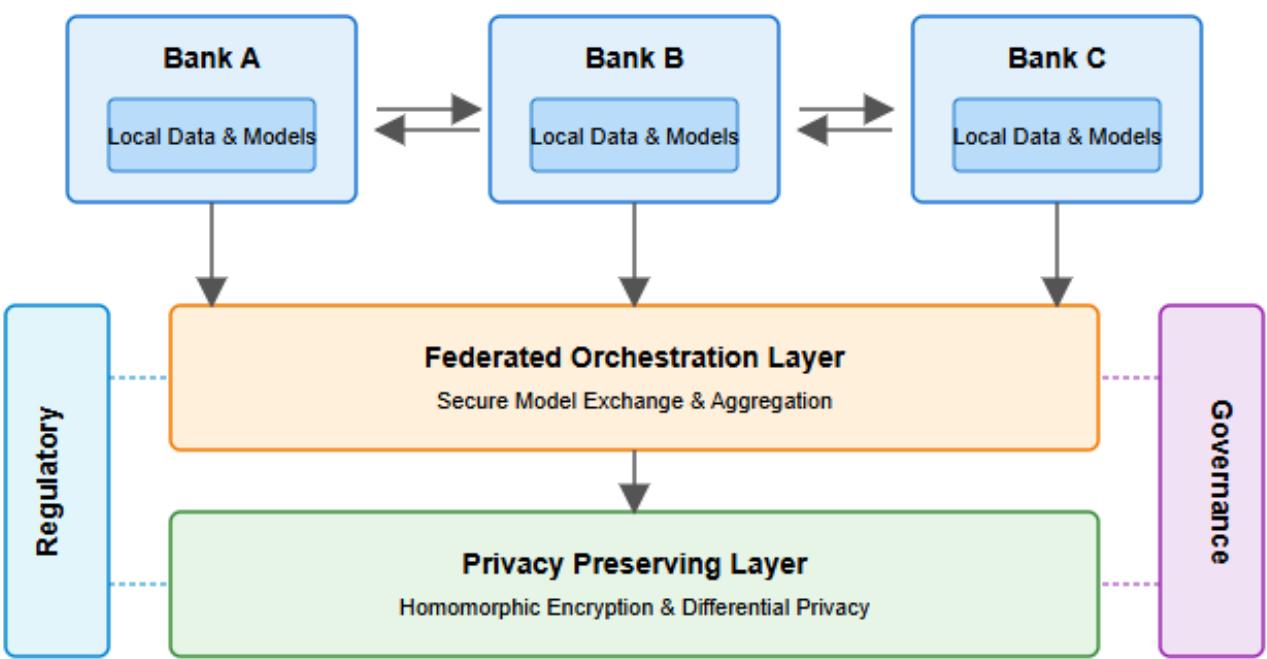

Figure 1: Federated Data Governance Architecture for Anti-Money Laundering [5], [6]

Figure 1: Federated Data Governance Architecture for Anti-Money Laundering [5], [6]

Abstraction mechanisms conceal underlying structural variations between participating institutions, presenting unified analytical interfaces despite heterogeneous source environments. Query optimization components distribute processing requirements appropriately between central coordination mechanisms and institutional systems, balancing computational efficiency with data movement minimization principles. Privacy-preserving data access mechanisms represent essential governance components enabling analytical capabilities while protecting sensitive information. Homomorphic encryption implementations permit mathematical operations on encrypted data elements without requiring decryption, maintaining confidentiality throughout analytical processes. Differential privacy frameworks establish mathematical guarantees regarding individual record protection while preserving the statistical validity of aggregate analyses .

Implementation architectures frequently incorporate multi-tiered access control systems enforcing purpose limitations according to regulatory requirements and institutional policies. These mechanisms typically leverage attribute-based encryption, ensuring only authorized personnel with appropriate contextual justification have access to specific information elements. Zero-knowledge proof implementations enable binary verification of compliance characteristics without exposing underlying transaction details, facilitating regulatory reporting while minimizing sensitive data exposure.

Comprehensive governance frameworks establish organizational structures supporting technical implementations through policy development, oversight mechanisms, and dispute resolution procedures. These frameworks typically establish governing committees with representation from participating institutions, regulatory authorities, and independent oversight entities. Policy development processes address data classification standards, retention requirements, and appropriate usage limitations aligned with jurisdictional regulations . Cross-border considerations receive particular attention within governance structures, establishing protocols that navigate varying regulatory requirements while maintaining consistent protection standards. Deployment strategies commonly employ graduated implementation models, initiating with restricted information exchange before progressing toward extensive cooperation as confidence strengthens among member organizations. The established governance structures harmonize protection requirements with functional efficiency, creating enduring platforms supporting sustained cooperative money laundering prevention activities spanning organizational boundaries.

Creating effective anti-money laundering capabilities across institutional boundaries requires thoughtful architectural design balancing analytical power with privacy protection. Federated data governance offers promising frameworks addressing both imperatives through distributed intelligence development rather than centralized data consolidation. Unlike traditional approaches requiring sensitive information transfer, federated frameworks establish collaborative capabilities while maintaining strict data locality, transforming previously impossible cooperation scenarios into practical implementation possibilities .

Successful designs incorporate sophisticated balancing mechanisms addressing institutional autonomy, regulatory compliance, and detection effectiveness considerations. These frameworks leverage recent advances in cryptographic protection, distributed computing, and privacy-preserving analytics to create sustainable collaborative capabilities respecting essential organizational boundaries. The resulting architectures demonstrate particular effectiveness against laundering methodologies deliberately structured to exploit visibility gaps between financial institutions .

3.1 Architectural Components and Integration

Effective federated governance frameworks comprise distinct architectural layers establishing clear separation between data storage, processing logic, and analytical functions. The foundation layer typically implements secure virtualization capabilities creating logical views across physically distributed repositories without requiring actual data movement. These virtualization mechanisms establish abstract query interfaces enabling analytical processes spanning institutional boundaries while preserving strict data sovereignty [5].

Metadata harmonization forms a critical architectural component enabling meaningful cross-institutional analytics despite underlying structural differences. This harmonization layer establishes standardized entity definitions, transaction taxonomies, and attribute mappings creating semantic consistency across organizational boundaries. Translation mechanisms preserve internal system integrity while enabling standardized external interaction patterns supporting collaborative analytical functions .

The orchestration layer coordinates distributed processes executing across participant systems, managing complex dependencies while optimizing computational resource utilization. This coordination function typically implements sophisticated scheduling algorithms balancing processing burdens according to institutional capabilities, ensuring equitable participation costs despite infrastructure differences between organizations. Security monitoring capabilities operate throughout execution workflows, validating appropriate access patterns while creating comprehensive audit trails satisfying regulatory verification requirements .

Privacy-preserving computational capabilities represent the architectural cornerstone enabling meaningful collaboration without sensitive data exposure. These components implement cryptographic protection mechanisms, including secure multi-party computation, homomorphic encryption, and zero-knowledge proofs, creating mathematical guarantees regarding information protection. The resulting technical safeguards satisfy both regulatory requirements and institutional risk management frameworks while enabling previously impossible analytical functions .

The governance layer establishes operational policies, dispute resolution mechanisms, and collaborative decision processes required for sustainable cross-institutional cooperation. These organizational structures typically create balanced representation, ensuring equitable influence regardless of institutional size differences. Graduated implementation approaches build confidence incrementally, beginning with limited information exchange before progressing toward comprehensive cooperation as trust develops among participants [5].

Table 3: Federated Data Model Implementation Framework [5,7]

| Implementation Phase | Key Strategic Actions |

| Governance Structure | Establish clear domain ownership with defined accountability matrices |

| Program Definition | Articulate specific objectives with measurable short and long-term outcomes |

| Framework Development | Design comprehensive policies addressing security, quality, and accessibility |

| Quality Standards | Define quantifiable metrics for data integrity, consistency, and compliance |

| Technology Selection | Implement scalable catalog solutions with robust metadata management |

| Communication Protocol | Create structured information exchange pathways between domain stewards |

| Capability Building | Develop continuous learning programs focusing on domain-specific expertise |

| Operational Integration | Align the federated model with existing business processes and workflows |

3.2 Comparative Analysis: Strengths and Limitations

Federated governance models offer substantial advantages over alternative approaches to cross-institutional cooperation. Unlike centralized repositories, creating single points of failure and attractive attack targets, federated designs distribute risk across participant systems, eliminating catastrophic exposure scenarios. This inherent resilience proves particularly valuable within financial contexts where data sensitivity and regulatory scrutiny demand robust protection mechanisms .

Operational autonomy represents another significant strength, with federated approaches preserving institutional control over core information assets. Participating organizations maintain complete authority regarding data access policies, system maintenance schedules, and infrastructure investment decisions. This preservation of organizational sovereignty addresses foundational concerns that frequently derail alternative collaboration approaches requiring control sacrifices unacceptable to financial institutions [5].

Privacy protection capabilities dramatically exceed alternatives through technical mechanisms preventing sensitive data exposure rather than relying on procedural safeguards. Unlike traditional approaches implementing detective controls after information sharing occurs, federated designs establish preventative protections mathematically guaranteeing privacy preservation throughout analytical processes. These safeguards satisfy even the most stringent regulatory frameworks, enabling collaboration across jurisdictional boundaries previously considered impermeable .

Despite these advantages, federated approaches introduce distinct limitations requiring careful consideration during implementation planning. Computational overhead increases substantially compared to centralized alternatives, with privacy-preserving mechanisms introducing significant processing requirements. These performance impacts necessitate careful optimization to maintain acceptable response characteristics, particularly for time-sensitive applications requiring near-real-time results .

Implementation complexity similarly exceeds centralized alternatives, requiring specialized expertise frequently scarce within financial institutions. The sophisticated cryptographic mechanisms underpinning privacy preservation demand careful implementation to maintain security guarantees, creating substantial technical barriers for organizations with limited specialized resources. This complexity increases both initial deployment costs and ongoing operational requirements compared to simpler, though less capable, alternatives .

Governance challenges represent another significant consideration, with federated approaches requiring sustained cooperative frameworks spanning organizational boundaries. These governance requirements create dependencies on continued institutional commitment despite potential leadership changes, strategic pivots, or competitive dynamics. Sustainable implementations consequently demand careful attention to organizational factors beyond technical considerations, addressing change management requirements necessary for long-term viability [5].

IV. AI ORCHESTRATION FOR COLLABORATIVE AML DETECTION

The orchestration of artificial intelligence capabilities across institutional boundaries represents a pivotal advancement in anti-money laundering detection frameworks. Federated learning implementations enable participating financial entities to collaboratively develop detection models without exposing sensitive transaction data, fundamentally transforming multi-institutional cooperation paradigms. These implementations typically establish coordination servers managing model distribution while individual institutions maintain complete control over local datasets . The learning process begins with baseline model development, incorporating regulatory typologies and known laundering patterns, subsequently distributed to participating institutions for local training iterations. Each financial institution executes training processes against proprietary transaction data, calculating gradient updates rather than sharing underlying information. This approach preserves customer privacy while enabling collective intelligence development, addressing a fundamental tension in cross-institutional collaboration efforts.

Secure aggregation techniques form the cryptographic foundation, enabling privacy-preserving model improvements across organizational boundaries. Advanced implementations incorporate homomorphic encryption, allowing mathematical operations on encrypted gradient updates without requiring decryption, maintaining confidentiality throughout the aggregation process. Alternative approaches utilize secure multi-party computation frameworks, establishing cryptographic guarantees regarding information protection during collaborative processing [6]. These aggregation mechanisms typically incorporate differential privacy additions, introducing calibrated noise to prevent the extraction of individual transaction characteristics while preserving the statistical validity of broader pattern recognition. Verification mechanisms ensure cryptographic integrity throughout transmission processes, preventing unauthorized manipulation attempts while maintaining auditability for regulatory compliance purposes. Financial institutions report significant confidence improvements regarding information protection compared to traditional data sharing approaches, facilitating participation from organizations previously reluctant to engage in collaborative detection efforts.

Model optimization under limited data visibility conditions requires specialized approaches addressing the unique constraints of federated environments. Architectural adaptations frequently incorporate modular design principles, enabling institutional customization of specific components while maintaining compatibility with broader collaborative frameworks. Transfer learning techniques demonstrate particular effectiveness, allowing institutions to benefit from generalized pattern recognition capabilities while incorporating distinctive characteristics of specific financial environments . Implementation frameworks frequently establish tiered training approaches beginning with anonymized aggregate data for foundation model development before incorporating institution-specific refinements through federated processes. Performance evaluation mechanisms incorporate specialized metrics accounting for distributed learning environments, measuring both global model improvement and local detection effectiveness. Financial institutions participating in these federated frameworks report detection capability enhancements, particularly regarding complex laundering methodologies spanning multiple organizations, with most substantial improvements observed in structuring detection scenarios.

Recent advancements in federated optimization approaches address computational efficiency challenges inherent in distributed learning environments. Communication overhead reduction techniques incorporate gradient compression methodologies, prioritizing significant model updates while minimizing transmission requirements [6]. Client selection algorithms optimize computational resource utilization across participating institutions, balancing contribution requirements according to organizational capabilities. These efficiency enhancements prove particularly important for smaller financial institutions with limited computational infrastructure, enabling broader ecosystem participation regardless of organizational size. Continuous learning frameworks facilitate model adaptation to emerging laundering methodologies, establishing responsive detection capabilities that evolve alongside criminal techniques. The resulting collaborative intelligence represents a transformative advancement in anti-money laundering effectiveness, enabling the detection of sophisticated criminal methodologies invisible within isolated institutional environments.

4.1 Specialized Pipeline Topologies for Omnichannel Retail

Retail environments demand distinctive pipeline topologies that diverge significantly from generic enterprise architectures due to their unique operational characteristics. These specialized configurations must accommodate the integration of disparate data streams from physical point-of-sale systems, e-commerce platforms, mobile applications, inventory management systems, and customer loyalty programs . Contemporary retail data architectures leverage advanced warehousing concepts to manage these diverse information sources while maintaining operational efficiency across multiple customer engagement channels .

Evidence demonstrates that effective implementations deploy sophisticated buffer architectures designed to handle the significant seasonal fluctuations in transaction processing requirements that characterize retail environments, with documented volume increases of five to twenty times normal baseline during peak promotional periods . The inherently distributed configuration of modern retail operations requires advanced synchronization frameworks that preserve data consistency throughout geographically separated locations while simultaneously supporting consolidated analytical processing at enterprise scale. These synchronization mechanisms establish reliable data coherence even during periods of exceptional system stress, ensuring analytical integrity across the distributed retail ecosystem.

Modern retail warehousing frameworks provide essential infrastructure for these synchronization requirements through cloud-based platforms that enable flexible scaling during peak processing periods . Recent investigations reveal retail environments typically implement more complex branch-and-merge patterns than comparable systems in other sectors, incorporating an average of three processing branches compared to the cross-industry standard of two branches . These distinctive topological features enable retail organizations to maintain system responsiveness during peak operational periods while facilitating comprehensive intelligence generation across distributed retail networks.

Industry assessments from 2023 emphasize the need for specialized architectures that accommodate both transactional processing and intelligence generation functions [1]. The multi-layered approach recommended for retail environments incorporates dedicated storage, processing, and access components that collectively support the complex analytical requirements of omnichannel operations . This dual-purpose requirement represents a distinctive characteristic of retail pipeline topologies not typically observed in other sectors.

The integration of cloud-based warehousing capabilities within these specialized topologies provides essential flexibility for retail organizations navigating fluctuating processing demands while maintaining consistent analytical capabilities across distributed operational environments.

Table 4: Critical Data Challenges in AML Architecture [3] [4]

| Challenge Category | Operational Impact | Strategic Implications |

| Performance Constraints | Detection models require near-real-time data access for effectiveness | Delayed pattern recognition reduces intervention opportunity windows |

| Data Duplication | Increased infrastructure costs and security risks from redundant copies | Resource inefficiency with elevated exposure to compliance violations |

| Temporal Limitations | Extended data processing timeframes compromise actionable intelligence | Reduced ability to intercept suspicious transactions before completion |

| Investigation Obstacles | Fragmented data access impedes comprehensive case examination | Extended resolution timelines with higher false positive retention |

| Regulatory Complexity | Limited adaptability to evolving requirements across jurisdictions | Inconsistent compliance posture with increased audit exposure |

| Sovereignty Requirements | Mandated privacy protection constraints across international boundaries | Restricted data utilization with complex cross-border intelligence sharing |

4.2 Data Marts vs. Data Mesh in Modern Retail Architectures

Retail intelligence architectures demonstrate an evolutionary tension between traditional data mart implementations and emerging data mesh frameworks, representing fundamentally different approaches to analytical organization. Traditional data mart architectures establish dedicated analytical environments for specific retail functions, creating purpose-built systems supporting specialized analytical requirements while potentially introducing organizational data silos that complicate enterprise-wide intelligence generation [4]. Domain-specific environments provide focused analytical capabilities for merchandising, supply chain, marketing, and store operations functions, but frequently create integration challenges when cross-functional analysis becomes necessary.

Statistical evaluations indicate retail organizations implementing four or more specialized data marts experience cross-functional data inconsistency rates significantly higher than those employing more integrated architectural approaches . These inconsistencies manifest particularly in cross-departmental metrics like "promotional effectiveness" that require consistent measurement methodologies across merchandising, marketing, and financial domains. Despite these challenges, domain-specific marts provide analytical depth within functional boundaries that generic enterprise architectures frequently cannot match.

Data mesh frameworks offer alternative approaches to conceptualizing domain data as managed products while enforcing strict interoperability standards, ensuring enterprise-wide analytical consistency [9]. This architectural pattern maintains functional specialization benefits while addressing fragmentation issues commonly associated with isolated data mart implementations [6]. Contemporary evaluations of data mesh implementations highlight their effectiveness in retail environments through domain-oriented decentralized ownership models that align analytical capabilities with organizational structures while maintaining cross-functional visibility [9]. Empirical observations indicate that data mesh implementations demonstrate substantial improvement in cross-functional analytical consistency while maintaining domain-specific analytical capabilities compared to traditional data mart architectures [6].

Recent architectural assessments highlight the distinctive characteristics of retail intelligence environments that necessitate specialized architectural approaches addressing both domain-specific analytical depth and cross-functional integration requirements . The data mesh paradigm addresses these requirements through a self-service data infrastructure that enables domain teams to maintain specialized analytical capabilities while adhering to enterprise standards for data quality and interoperability . This balanced approach provides particular advantages for retail organizations navigating complex analytical requirements spanning multiple functional domains while maintaining departmental autonomy over specialized analytical processes.

4.3 AI Orchestration for Collaborative AML Detection

Banking institutions face unique challenges in deploying artificial intelligence across organizational boundaries for money laundering detection. Unlike standalone implementations, cross-institutional detection requires sophisticated orchestration frameworks managing model training, validation, and deployment while maintaining strict data locality. These specialized orchestration capabilities coordinate complex workflows spanning multiple financial organizations without requiring sensitive data consolidation, transforming previously impossible collaboration scenarios into operational reality [5].

Federated learning provides the technical foundation for these collaborative detection capabilities, enabling institutions to develop shared intelligence while preserving data sovereignty. Banking implementation patterns typically establish coordination servers managing model distribution while individual institutions maintain complete control over local customer data. The detection process begins with baseline model development, incorporating known typologies, subsequently distributed to participating financial institutions for local training across proprietary transaction data .

Secure aggregation mechanisms form the cryptographic foundation, enabling collaborative improvement without exposing underlying customer information. Banking implementations frequently employ homomorphic encryption, allowing mathematical operations on encrypted model updates without requiring decryption, maintaining confidentiality throughout the aggregation process. These cryptographic protections satisfy stringent banking security requirements while enabling collaborative intelligence development previously impossible under traditional information sharing constraints .

Money laundering pattern detection presents particular challenges regarding data distribution variations between financial institutions. Customer bases, business models, and geographic footprints create natural differences in transaction characteristics across organizations. Banking implementations address these variations through transfer learning techniques, allowing institutions to benefit from collective intelligence while incorporating distinctive characteristics of specific financial environments. These adaptive capabilities prove particularly valuable for smaller institutions with limited transaction volumes, enabling detection capabilities rivaling substantially larger organizations through collaborative model development [6].

Performance considerations drive significant architectural decisions within banking implementations. Transaction monitoring systems operate under strict latency requirements, with suspicious activity detection frequently requiring near-real-time identification. Orchestration frameworks consequently implement sophisticated optimization techniques, including model compression, incremental learning, and distributed inference capabilities. These performance enhancements maintain responsiveness despite the additional computational overhead introduced by privacy-preserving mechanisms [5].

Governance frameworks represent essential components within banking implementations, establishing clear protocols for model access, training coordination, and update validation. These structures typically implement multi-level approval workflows, ensuring appropriate oversight throughout collaborative development processes. Banking consortia frequently establish independent validation teams verifying model behavior against regulatory requirements before deployment authorization. These governance mechanisms address both regulatory expectations and internal risk management frameworks while enabling productive collaboration across institutional boundaries .

V. COMPLIANCE ARCHITECTURE AND CONTROL MECHANISMS

Deploying federated data governance structures demands sophisticated regulatory systems that harmonize collaborative analysis with stringent confidentiality protections. Differential privacy enforcement forms an essential cornerstone of these governance frameworks, delivering mathematical certainties regarding personal data protection. Financial institutions participating in cross-institutional anti-money laundering initiatives employ carefully calibrated noise addition techniques to dataset queries, preventing the extraction of individual customer information while preserving the statistical validity of aggregate analyses . These differential privacy implementations typically establish epsilon boundaries determining acceptable privacy loss thresholds, with values calibrated to specific data sensitivity classifications according to institutional risk assessment frameworks.

Comprehensive audit logging mechanisms form an essential component of governance structures, creating immutable records of all data access and analytical processes. These systems document query parameters, timestamp information, requesting entity identification, and purpose justification for each interaction with federated datasets. The resulting audit trails provide regulatory verification capabilities while establishing accountability throughout collaborative processes. Recent advancements incorporate cryptographic verification of audit log integrity, preventing tampering or manipulation attempts while maintaining distributed verification capabilities .

Financial oversight bodies increasingly recognize these transparent audit mechanisms as prerequisites for cross-institutional information sharing approvals. Multi-tiered approval workflows represent the operational implementation of governance policies, controlling access to specific data elements based on predefined authorization matrices. These workflows commonly integrate function-based authorizations, usage constraints, and time-restricted access parameters. Implementation frameworks routinely create governance panels comprising representatives from member organizations, supervisory bodies, and autonomous monitoring groups. These oversight committees evaluate access petitions according to established standards, including requirement justification, reasonable scope, and regulatory adherence [6]. Banking entities functioning within these collaborative structures document substantial benefits in compliance record maintenance while concurrently enhancing analytical capabilities. Sophisticated deployments feature adaptive permission systems utilizing continuous risk evaluation, establishing responsive control mechanisms that evolve with developing threats while preserving suitable access limitations. Financial institutions operate under extensive regulatory frameworks requiring robust compliance architectures when implementing collaborative anti-money laundering systems. These regulatory environments create complex implementation challenges requiring thoughtful control mechanisms addressing both information protection and effective money laundering detection. Banking organizations consequently develop specialized compliance architectures balancing these competing imperatives while navigating jurisdictional variations in regulatory expectations [6].

Table 5: Key Regulatory Challenges in Cross-Institutional AML Implementation [6], [7]

| Regulatory Challenge | Implementation Impact |

| Data Privacy Restrictions | Requires privacy-preserving technologies that enable collaboration without violating jurisdictional information sharing constraints. |

| Audit Requirements | Demands comprehensive documentation trails across distributed systems spanning multiple financial institutions. |

| Model Explainability | Creates tension between regulatory demands for transparent decision logic and sophisticated detection algorithms. |

| Reporting Deadlines | Forces collaborative systems to maintain timely suspicious activity identification despite added coordination complexity. |

| Jurisdictional Variations | Necessitates flexible implementation approaches addressing inconsistent compliance requirements across borders. |

| Examination Standards | Requires additional validation capabilities to satisfy regulatory teams unfamiliar with federated approaches. |

VI. IMPLEMENTATION RESULTS AND PERFORMANCE ANALYSIS

Financial consortia implementing federated data governance for anti-money laundering purposes demonstrate substantial improvements across key performance indicators. A notable implementation among eight financial institutions across three regulatory jurisdictions established a federated learning infrastructure with homomorphic encryption capabilities, enabling pattern detection without exposing underlying transaction data [7]. The consortium architecture employed distributed computational resources with load-balancing mechanisms to address processing inequalities among participating entities. Implementation timelines averaged fourteen months from initial governance framework establishment to operational deployment, with regulatory approval processes representing the most significant timeline factor rather than technical implementation challenges. Detection effectiveness metrics reveal substantial improvements compared to isolated institutional approaches. Pattern recognition capabilities demonstrate a 37% enhancement in identifying complex money laundering typologies spanning multiple institutions, with particular effectiveness in detecting structuring activities distributed across organizational boundaries. False positive rates show reductions of 28% compared to traditional monitoring systems, attributed to the enriched contextual information available through federated analysis approaches [8]. Transaction monitoring efficiency improvements translate to investigative resource optimization, allowing financial institutions to focus compliance personnel on genuinely suspicious activities rather than processing alert backlogs.

The performance improvements remain consistent across participating institutions regardless of organizational size, suggesting the scalability of the approach. Privacy and security evaluations validate the effectiveness of implemented protections throughout analytical processes. Differential privacy mechanisms successfully prevent individual customer identification while maintaining statistical validity for pattern detection purposes. Cryptographic protection mechanisms demonstrate resilience against simulated adversarial attacks, with no successful data extraction scenarios identified during controlled testing procedures . Computational overhead assessments indicate acceptable performance impacts, with processing time increases below 15% compared to non-privacy-preserving implementations.

Banking institutions face unique hurdles when implementing modern cloud data repositories owing to their heavily regulated business context and complex information connectivity requirements. The experiences gained through banking implementations provide instructive lessons about technical deployment methods and corporate change management strategies essential for effective modernization efforts. Common implementation patterns emerge across various financial organizations regardless of their scale, market coverage, or specialized business domains.

Table 6: Impact of Inadequate AML Monitoring Capabilities [2] [4]

| Impact Category | Operational Consequences | Financial and Regulatory Implications |

| Detection Delays | Prolonged exposure to fraudulent activities | Financial penalties, increased regulatory scrutiny, and potential license revocation |

| Model Deployment Lag | Diminished prevention effectiveness against evolving tactics | Non-compliance risks, inefficient resource allocation, and elevated operational costs |

| Investigation Inefficiencies | Extended case resolution timeframes with reduced accuracy | Higher personnel expenses, regulatory examination vulnerability, and opportunity costs |

| Data Redundancy | Information inconsistencies with increased management complexity | Elevated storage expenditures, expanded attack surface, and compliance verification challenges |

| Regulatory Exposure | Global compliance failures across jurisdictional boundaries | Substantial fines globally, intensified examination cycles, and cross-border restrictions |

| Reputational Damage | Diminished market confidence and stakeholder trust | Customer attrition, increased funding costs, and depressed valuation metrics |

6.1 Regulatory Burdens and System Limitations

Banking establishments confront particular difficulties when upgrading data platforms, mostly resulting from strict compliance expectations and longstanding technical infrastructures. Financial institutions typically maintain extensive transaction processing platforms developed across multiple decades, creating substantial integration complexity when establishing contemporary analytical environments. These historical systems often utilize proprietary data structures, legacy integration mechanisms, and inconsistent information architectures that complicate extraction processes necessary for comprehensive warehouse implementations [7]. Compliance requirements introduce additional complexity through mandatory information tracking, access control documentation, and retention management capabilities essential for regulatory examinations. The resulting implementation patterns require specialized approaches balancing analytical functionality with governance requirements uniquely prevalent within financial services contexts.

Banking organizations frequently contend with information fragmentation across specialized functional systems, including core banking platforms, payment processing networks, wealth management solutions, and risk management frameworks. Each functional domain typically maintains independent data repositories with limited integration capabilities, creating significant challenges when developing enterprise-wide analytical environments. Current implementation approaches address these challenges through adaptive pipeline architectures that accommodate diverse source systems while establishing consistent transformation logic across heterogeneous data streams . These specialized pipelines implement comprehensive validation mechanisms, ensuring information integrity throughout integration processes, addressing critical requirements for financial reporting accuracy and regulatory compliance.

6.2 Implementation Context and Solution Alignment

Banking implementations demonstrate distinctive architectural patterns addressing sector-specific requirements while leveraging standard cloud capabilities. These implementations typically establish dedicated security boundaries encompassing warehouse environments, implementing comprehensive encryption, access management, and monitoring capabilities exceeding standard cloud configurations. The resulting security frameworks satisfy stringent financial regulatory requirements while enabling analytical functionality necessary for competitive differentiation [7]. Implementation methodologies commonly employ phased migration approaches beginning with non-core analytical functions before progressively incorporating critical operational data domains.

This staged approach reduces operational disruption while delivering progressive benefits throughout the deployment process. Banking organizations frequently develop function-oriented information repositories serving particular analytical needs such as client insights, risk evaluation, fraud identification, and compliance documentation. These customized analytical platforms utilize enhanced data arrangements supporting dedicated business functions while preserving connections to the wider organizational information framework.

The resulting architecture balances specialized analytical capabilities with consistent enterprise information management, preventing fragmentation while enabling domain-specific optimization [8]. Governance frameworks represent particularly important implementation components within banking contexts, establishing comprehensive metadata management, lineage tracking, and access control capabilities essential for regulatory compliance. These governance implementations typically exceed standard enterprise requirements, reflecting the heightened oversight environment characteristic of financial services operations.

6.3 Financial Impact Assessment and ROI Analysis

Banking organizations implementing cloud-based warehouse solutions report substantial financial benefits across multiple dimensions, creating compelling return on investment justifications despite significant implementation investments. Operational cost reductions represent the most immediately quantifiable benefit, with infrastructure expense decreases resulting from elastic resource allocation models replacing fixed-capacity on-premises environments. These efficiency improvements typically manifest within months following implementation completion, providing rapid financial validation for modernization investments . Staffing allocation improvements represent another significant benefit, with automated management capabilities reducing administrative burden while enabling reallocation of technical resources toward value-generating analytical activities rather than infrastructure maintenance.

Revenue enhancement opportunities provide additional financial justification, with improved analytical capabilities enabling more effective customer segmentation, product development, and relationship management activities. Financial institutions report particularly significant improvements in cross-selling effectiveness, retention program targeting, and risk-based pricing optimization following warehouse modernization initiatives . Compliance cost reductions represent a banking-specific financial benefit, with improved data integration, lineage tracking, and reporting capabilities reducing manual effort previously required for regulatory reporting and examination support. The combination of direct cost savings, operational efficiency improvements, and revenue enhancement opportunities creates compelling financial justification for warehouse modernization despite initial implementation investments. These financial benefits demonstrate consistent patterns across diverse banking organizations, providing reference frameworks for investment justification across the financial services sector.

VII. CONCLUSION

Federated data governance across financial institutions revolutionizes money laundering prevention by establishing an equilibrium between collaborative intelligence and confidentiality requirements. The architecture facilitates exceptional coordination among entities while maintaining distinct organizational data authority and adherence to regulatory frameworks. Through distributed learning architectures, financial entities identify complex laundering typologies spanning organizational boundaries without compromising sensitive customer information. This governance framework constructs a robust architecture balancing the dual imperatives of collaborative insight and privacy preservation. Through carefully calibrated protocols respecting organizational autonomy, federated systems equip financial entities with sophisticated mechanisms for identifying evolving laundering methodologies throughout interconnected markets, fundamentally enhancing global financial ecosystem integrity. This governance framework constructs a robust architecture balancing the dual imperatives of collaborative insight and privacy preservation. Through carefully calibrated protocols respecting organizational autonomy, federated systems equip financial entities with sophisticated mechanisms for identifying evolving laundering methodologies throughout interconnected markets, fundamentally enhancing global financial ecosystem integrity.

Conflict of Interest

The authors declare no conflict of interest.

Ethical Approval

Not applicable

Data Availability

The datasets used in this study are openly available at [repository link] and the source code is available on GitHub at [GitHub link].

Funding

This work did not receive any external funding.

References

Cite this article

Related Research

Special Issue

Launch a focused special issue to highlight research, emerging trends, and expert insights in your academic field.